How much church tax will I save if I leave the church?

If you were to leave the church, you would not actually save the full amount of church tax deducted from your salary over the year. You would also have to forgo the benefit of deducting the church tax as special expenses from your taxable income.

You are entitled to a flat rate allowance for special expenses of 36 Euro for the whole year (72 Euro for couples). However, you can claim the full amount of church tax as special expenses. This reduces your taxable income and also your income tax.

Example: If you and your spouse pay 600 Euro in church tax per year, you can additionally claim the amount exceeding the flat rate allowance for special expenses as special expenses (600 Euro church tax minus 72 Euro flat rate allowance for special expenses).

528 Euro at a marginal tax rate of 28 percent will give you back 147 Euro in income tax. This reduces your church tax, which is calculated based on income tax, as well as the solidarity surcharge (9 percent or 5.5 percent of 147 Euro). This amounts to around 20 Euro less. Thus, the church tax gives you a tax advantage of a total of 167 Euro.

You would therefore have to deduct this special expenses advantage from your church tax to calculate what leaving the church would save you. In this example, as a couple, you would save 433 Euro compared to the previous year if you do not pay church tax, but you would also have to forgo the option of deducting special expenses.

(2023): How much church tax will I save if I leave the church?

The "special church contribution": Obligation to pay church tax for a non-denominational spouse.

Church tax liability generally applies only to members of a religious community that collects taxes who have their residence in Germany and within the area of this religious community. The decisive factor is formal membership, not the intensity of faith or participation in religious life. Anyone who does not belong to a religious community that collects taxes does not have to pay church tax. But does this also apply to spouses?

It is not uncommon for the well-earning spouse to leave the church to save on church tax, while the non-working spouse and children remain members of the church community. However, those who believe that no church tax needs to be paid at all could be mistaken.

If the church member spouse has no income of their own, no "church tax on income" can be levied. However, in mixed-faith marriages, the churches levy the "special church fee" as a special form of church tax, which is mainly used by the Protestant churches.

- The "special church fee" is demanded from the church member spouse who has little or no income and therefore does not have to pay church tax on income. In this case, the special church fee is based on the joint taxable income of both spouses. It is only levied if the joint taxable income is higher than 30.000 Euro, and only in the case of joint assessment, not in the case of individual assessment for spouses.

- According to the Federal Constitutional Court, it is constitutionally acceptable for the "special church fee" to be based on the living expenses of the church member spouse. In the case of joint assessment, the joint taxable income is used as an auxiliary measure. The levying of the special church fee is permissible, even if the income is only earned by the other - non-religious - spouse. In marriage as a living and economic community, each spouse has a half share in the income of the other (Federal Constitutional Court decision of 28.10.2010, 2 BvR 591/06).

The European Court of Human Rights (ECHR) has recently ruled that the collection of church tax or the special church fee in a mixed-faith marriage in Germany does not violate the European Convention on Human Rights and is therefore permissible (ECHR decision of 6.4.2017, complaint no. 10138/11 et al.).

The case: The claimant does not belong to any religious community, his wife is a member of the Protestant Church. The couple applies for joint assessment - with the result that the man has to pay his wife's church tax of 2.220 Euro. This amount was deducted from a tax refund. He and four other complainants therefore argued before the ECHR that

- the assessment of the church tax or church fee based on the joint income of spouses violated their rights under Art. 9 ECHR (freedom of religion) in several respects,

- they were required to pay the special church fee for their spouse without being a member of a church themselves,

- they were dependent on financial support from their spouse to pay the church fee and were therefore dependent on their spouse in exercising their freedom of religion,

- they were obliged to pay a disproportionately high church tax because the income of the spouse was also taken into account in its assessment.

The Saxon Finance Court currently considers the regulation in Saxony on the special church fee in mixed-faith marriages to be incompatible with the Basic Law, as spouses were disadvantaged without objective reason compared to registered civil partnerships in 2014 and 2015. The regulation violated the general principle of equal treatment (decision of 25.3.2019, 5 K 1549/18).

The Bavarian State Ministry of Finance has recently announced that in Bavaria the Evangelical Lutheran Church and the Evangelical Reformed Church will waive the collection of the special church fee, retroactively from the 2018 tax year (decree of the Bavarian State Ministry of Finance of 21.1.2019, BStBl I 2019 p. 213).

Das besondere Kirchgeld

The special church fee comes into play when one spouse does not belong to a church that collects taxes and the other church tax-liable spouse

- does not earn their own income,

- earns their own income that does not trigger income tax and therefore no church income tax due to its low amount, or

- earns their own income that already triggers church tax, but as a result of the so-called comparison calculation leads to the assessment of a higher special church fee.

The Federal Finance Court has recently pointed out that even in the third case group, the assessment of the special church fee is constitutionally acceptable, although church tax is already due based on the individual's income (Federal Finance Court decision of 5.10.2021, I B 65/19). The Federal Finance Court refers to decisions of the Federal Constitutional Court (e.g. Federal Constitutional Court decision of 28.10.2010, 2 BvR 591/06).

No separate justification is required in this case group. The living expenses of the church tax-liable spouse increase "if they have their own income, but the spouse has a significantly higher income" (Cologne Finance Court ruling of 8.6.2005, 11 K 1389/03).

It is also obvious that the permissibility of levying the special church fee in this case group requires a regulation to clarify the relationship between the special church fee and the church income tax; e.g. a regulation to avoid double taxation with both types of tax. Corresponding credit regulations or comparison calculations are included in the state legal or church tax regulations. They are legally unproblematic and have therefore not been objected to by the specialised courts or the Federal Constitutional Court.

Conclusion: Even in the third case group, the living expenses of the church member spouse may be taxed by means of the special church fee. For the sake of completeness, it should be noted that the special church fee is not levied uniformly throughout Germany.

(2023): The "special church contribution": Obligation to pay church tax for a non-denominational spouse.

How can I reduce my church tax by claiming child benefit?

The amount of church tax depends on your place of residence. If you live in Bavaria or Baden-Württemberg, church members pay 8 percent; in other states, it is 9 percent. The basis is the assessed income tax. You therefore pay 8 or 9 percent of your income tax as church tax.

Please note: The church tax is also taken into account at the same percentage rate within the withholding tax. If child allowances are entered in employees' electronic payslip data (ELStAM), the monthly church tax is calculated based on a so-called fictitious wage tax.

Church tax without child allowance:

You live in Berlin and have a gross monthly salary of 3.000 Euro in tax class IV. Your monthly church tax is 31.44 Euro. Church tax with two child allowances: You live in Berlin and have a gross monthly salary of 3.000 Euro in tax class IV. Your monthly church tax is now 13.34 Euro.

If a "number of child allowances" is entered in the ELStAM, the monthly wage tax is not reduced, only the monthly church tax and the monthly solidarity surcharge. This also applies if you receive child benefit during the year.

In the income tax assessment, child allowances only reduce the taxable income if the child benefit is not more favourable than the tax advantage. However, for the calculation of church tax (and solidarity surcharge), the child allowances are deducted "fictitiously".

Advantage: Even if children are only to be considered for part of the year, the full child allowance and BEA allowance are always deducted for the calculation of church tax and the solidarity surcharge. This applies in the case of the end of vocational training or the birth of a child.

(2023): How can I reduce my church tax by claiming child benefit?

When am I required to pay church tax?

The church tax obligation begins with baptism or upon joining or rejoining the religious community. In this case, you must pay the church tax from the beginning of the following month.

If you change religious communities, the obligation to pay church tax also begins at the start of the following month. However, it only starts once you no longer pay church tax to your previous religious community.

In the Israelite religious community, the church tax obligation is based on descent and faith.

(2023): When am I required to pay church tax?

Who is required to pay church tax?

If you are a member of one of the following religious communities, you must pay church tax:

- Roman Catholic Church

- Protestant Churches

- Old Catholic Church

- Jewish Communities

- Israelite Religious Communities (e.g. in Baden-Württemberg)

- Free Religious Communities (e.g. in Baden, Württemberg, Mainz, Offenbach, Palatinate)

- French Church in Berlin (Huguenot Church)

- Mennonite Congregation in Hamburg-Altona

- Unitarian Religious Community of Free Protestants in Rhineland-Palatinate

The amount of church tax depends on your place of residence. If you live in Bavaria or Baden-Württemberg, you pay 8 percent, in other states 9 percent of income tax or wage tax.

(2023): Who is required to pay church tax?

How much is the church tax?

The amount of church tax depends on your place of residence. If you live in Bavaria or Baden-Württemberg, church members pay 8 percent; in other federal states, it is 9 percent. The basis is the assessed income tax. You therefore pay 8 or 9 percent of your income tax as church tax.

Please note: The church tax is also taken into account at the same percentage rate within the withholding tax.

If you have children or if your taxable income (zvE) includes income from business operations and/or income taxed under the so-called partial income procedure, the zvE is calculated separately for church tax purposes.

If child allowances are entered in employees' electronic wage tax deduction features (ELStAM), the monthly church tax is calculated based on a so-called fictitious wage tax.

Example

You live in Berlin and have a gross monthly salary of 3.000 Euro in tax class IV. Your monthly church tax is 34,31 Euro. Church tax with two child allowances: You live in Berlin and have a gross monthly salary of 3.000 Euro in tax class IV. Your monthly church tax is now 16,74 Euro.

If a "number of child allowances" is entered in the ELStAM, the monthly income tax is not reduced, only the monthly church tax and the monthly solidarity surcharge. This also applies if you receive child benefit during the year.

In the income tax assessment, child allowances only reduce the taxable income if the child benefit is not more favourable than the tax advantage. However, for the calculation of church tax and solidarity surcharge, the child allowances are "fictitiously" deducted.

Advantage: Even if children are only to be considered for part of the year, the full child allowance and BEA allowance are always deducted for the calculation of church tax and solidarity surcharge. This applies in the case of the end of vocational training or the birth of a child.

(2023): How much is the church tax?

When can I deduct church tax as special expenses?

If you are a member of a church, you can deduct the church tax as special expenses. Prepaid or additional church tax payments can also be claimed for tax purposes.

If you are a member of a religious community that does not levy church tax, you can deduct payments to them “as church tax” – i.e. 8 or 9 percent of income tax, depending on the federal state. However, the church must be recognised as a public corporation in at least one federal state. A receipt is required. Examples of such religious communities include the New Apostolic Church, the Evangelical Free Churches, the Greek Orthodox Metropolis, the Independent Evangelical Lutheran Church, the Methodist Episcopal Church, the Salvation Army, and Jehovah's Witnesses.

Payments exceeding the corresponding church tax can be claimed as donations for church purposes.

Under new legislation, church tax payments to religious communities in an EU/EEA state are also recognised as special expenses.

If the religious community is not recognised as a public corporation, you can deduct your contributions as donations to "promote religious purposes" up to 20 percent of the total income. You must enter this information in the “Donations” section. This applies, for example, to the Old Buddhist Community.

The Scientology Church is not a religious community.

(2023): When can I deduct church tax as special expenses?

From when do you no longer have to pay church tax after leaving the church?

Church tax liability ends:

- at the end of the calendar month if the residence or usual place of abode in Germany has been given up.

- at the end of the month of death if the church member dies.

- when the church member declares their resignation from the church. Different authorities are responsible for the declaration of resignation in the various federal states; in most cases, it is made at the registry office, otherwise at the local court; only in the state of Bremen also at the church. Depending on the federal state, the resignation is effective from the calendar month in which it was declared, or from the following calendar month.

Note

In the past, there was a so-called "month of remorse" in some federal states, meaning church tax liability ended one month after the month of resignation. This applied to Berlin, Brandenburg, Bremen, Hamburg, Hesse, Mecklenburg-Western Pomerania, Saxony, Schleswig-Holstein, Thuringia.

However, the month of remorse has now been abolished to standardise church tax regulations across the country, meaning the resignation takes effect in the calendar month in which it is declared.

After resigning from the church, the registration office automatically informs the relevant tax office so that it can change the electronic wage tax deduction features (ELStAM). Therefore, no church tax will be deducted from your monthly salary after your resignation.

Cost of resigning from the church - resignation fees

In Berlin, Brandenburg and Bremen, resignation is free of charge. In other federal states, you must pay between 10 and 60 Euro for the certificate of resignation.

(2023): From when do you no longer have to pay church tax after leaving the church?

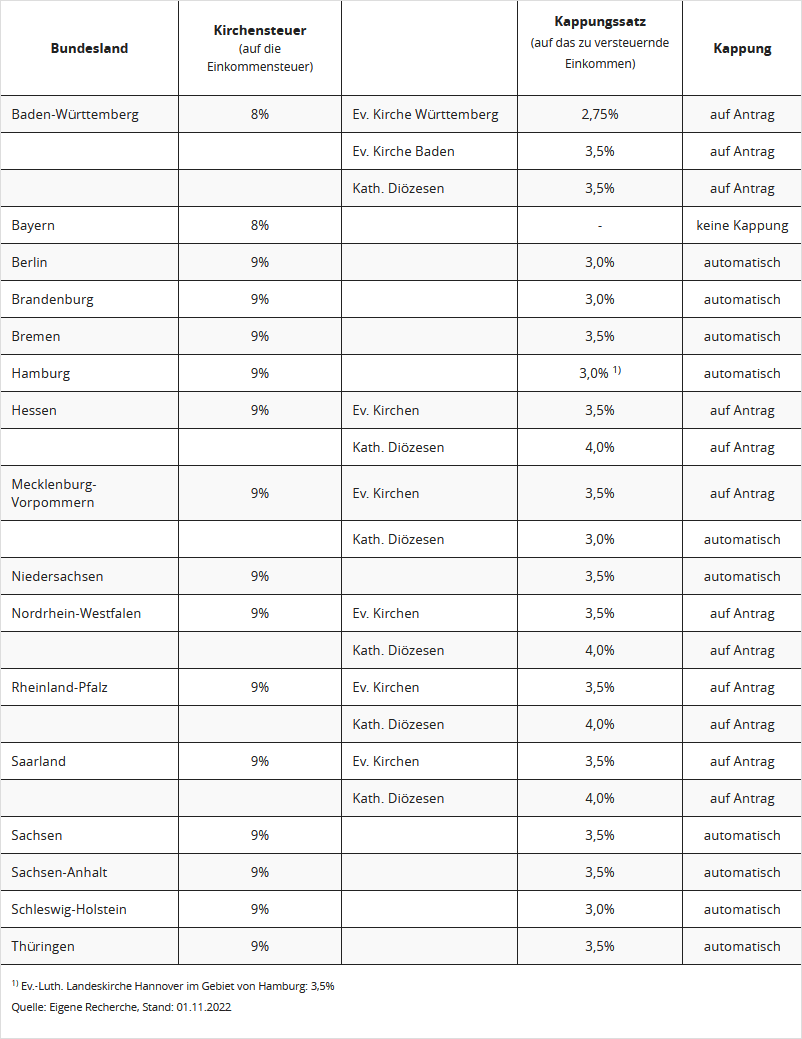

What is the advantage of capping the church tax?

The amount of church tax depends on your place of residence. If you live in Bavaria or Baden-Württemberg, you pay 8 percent; in the other federal states, 9 percent. The basis is the assessed income tax. So you pay 9 percent of your income tax as church tax.

The higher your income, the higher the income tax and thus the higher the church tax. However, there is the option to apply for a cap on the church tax. This means: The church tax is no longer calculated based on the "income tax" but on the "taxable income". The capping rate varies between federal states and is between 2.75 and 4 percent of the taxable income.

Most church tax laws provide for a cap on income tax for high incomes. However, you should check whether the cap is granted automatically or only upon application in your federal state. There are different regulations:

- A cap without application is automatic in the federal states of Berlin, Brandenburg, Bremen, Hamburg, Mecklenburg-Western Pomerania, Lower Saxony, Saxony, Saxony-Anhalt, Schleswig-Holstein, and Thuringia.

- The cap only with application is available in Baden-Württemberg, Hesse, North Rhine-Westphalia, Rhineland-Palatinate, and Saarland.

- In Bavaria, no cap on church tax is possible.

Check whether a cap is already beneficial for your income. If so, submit an (informal) application for a cap on the church tax (plus a copy of the latest tax assessment) to your diocese or regional church.

Example:

In Berlin, a capping rate of 3 percent applies. So the church tax is limited to 3 percent of the taxable income.

2023 taxable income: 150.000 Euro

income tax payable under the basic rate: 53.027 Euro

church tax payable (9 percent): 4.772 Euro.

With a cap of 3 percent of the income, only 4.500 Euro church tax would have to be paid.

(2023): What is the advantage of capping the church tax?