When are pensioners required to submit a tax return?

A pensioner is required to submit a tax return 2022 if their total income exceeds the annual personal allowance. In 2021, the personal allowance is 9,744 Euro for single persons and 19,488 Euro for married couples.

Taxable income for pensioners that must be declared includes private and state pensions (Form R), as well as rental and capital income (Form V and Form KAP), among others.

Not every Euro of the state pension is part of a pensioner's taxable income. This means that someone receiving a state pension of 1,500 Euro per month does not have to pay tax on the entire annual sum of 18,000 Euro. The actual amount of the taxable pension depends on the year the employee retired. The taxable portion is 50% of the pension amount for all pensioners from 2004 and for those who retired in 2005, regardless of age. Those who retired in 2006 had to pay tax on 52% of the pension amount. For retirement in 2021, the taxable portion is 81%, and for retirement in 2022, it is 82%.

The taxable portion is applied only in the year of retirement and the second year of receiving the pension. The remaining amount in the second year is the personal pension allowance, which remains tax-free for life. From the third year onwards, the pension is fully taxable after deducting the personal pension allowance and the standard allowance for income-related expenses of 102 Euro. The constant pension allowance means that pension increases from the third year onwards are fully taxable.

Example: For Manfred Mustermann, who retired in 2005, the taxable pension is 50%. Like all pensioners who retired by 2005, he receives an allowance of 50%. This is not taxable and remains unchanged for life.

For Mr Mustermann: If he received a pension of 30,000 Euro in 2005, his allowance is 15,000 Euro. This annual allowance remains constant until the end of his life. The married pensioner Mustermann and his wife have no other income. Therefore, they do not have to submit a tax return, as their income is below the personal allowance of 20,694 Euro (2022). If Max Mustermann were single, it would be different. With a taxable annual pension of 15,000 Euro, he would be above the personal allowance of 10,347 Euro (2022) and would therefore have to submit a tax return. If both spouses are above the personal allowance, they must each submit a separate form.

Tip

Pensioners who have to submit a tax return should also ensure that they claim possible income-related expenses.

(2022): When are pensioners required to submit a tax return?

What is the retirement relief amount?

The old-age relief amount can be used by pensioners who, in addition to income from pensions, also earn additional income or wages.

Additional income includes, for example:

- Income from renting,

- Capital assets,

- Income from self-employment,

- Income from private sales transactions,

- Income from a Riester pension.

However, the tax office first deducts various amounts (saver's allowance, income-related expenses allowance). The amount of the old-age relief depends on the pensioner's year of birth.

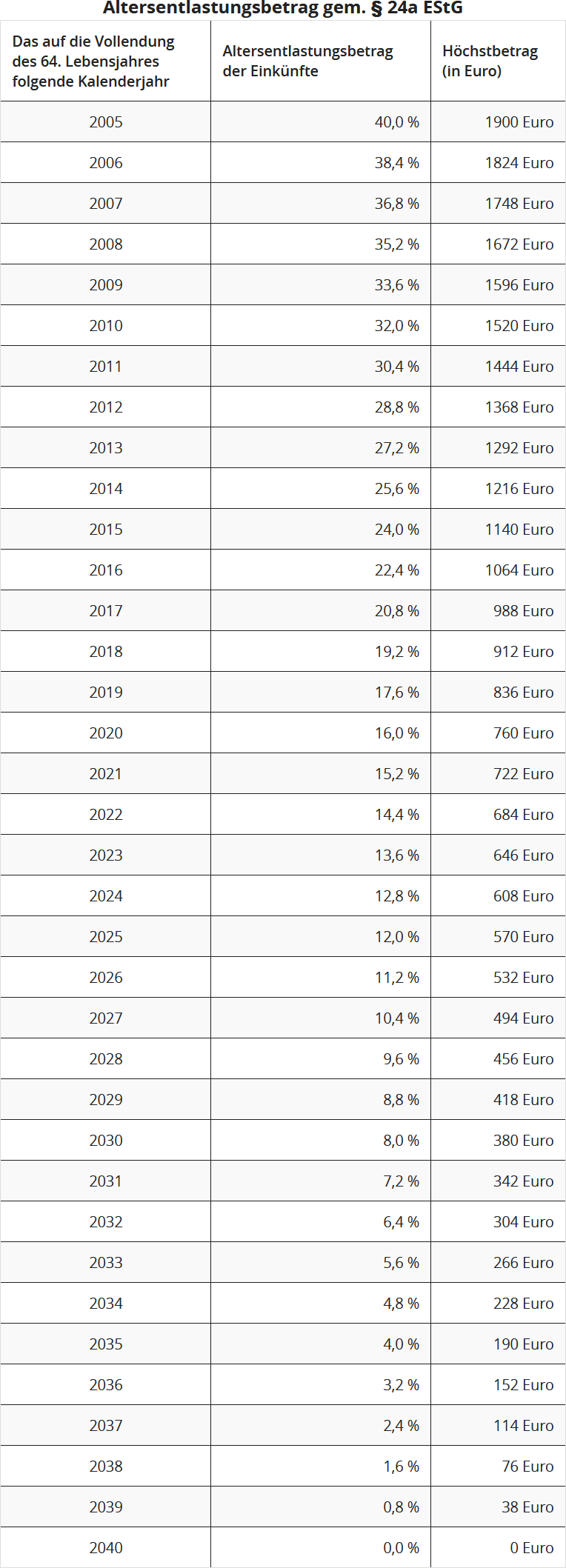

If you turn 64 in 2022 (born between 2.1.1958 and 1.1.1959), the old-age relief from 2023 is 13.6%, up to a maximum of 646 Euro.

The relevant percentages and maximum amounts for the old-age relief depend on the calendar year following the 64th birthday. These amounts are then fixed for life.

(2022): What is the retirement relief amount?

Which pensions must be declared in the tax return?

Pensions are generally subject to income tax. There are different tax rules:

- Pensions taxed with the new taxable portion, more precisely: fully taxable after deduction of the personal pension allowance. This applies to all pensions from the statutory pension insurance, the "Rürup" pension, and pensions from professional pension schemes.

- Pensions taxed with the favourable yield percentage. This applies, for example, to pensions from private pension insurance.

- Pensions taxed with the special yield percentage according to § 55 EStDV. This applies to life annuities with a fixed term, e.g. occupational or disability pensions from private insurance.

- Pensions fully taxable as "other income". This mainly concerns the state-subsidised Riester pension and the non-compliant use of Riester contracts, as well as benefits from occupational pensions whose contributions remained tax-free, e.g. from pension funds, pension schemes, and direct insurance.

- Pensions fully taxable as "income from employment". This applies to civil service pensions, company pensions from a direct commitment or support fund, as well as corresponding survivor benefits. These pensions are not to be entered in "Anlage R", but in "Anlage N".

- Pensions that are fully tax-free, e.g. pension from statutory accident insurance. You do not need to declare these pensions in the tax return.

Pensions belong in Anlage N

Pensions, e.g. company pensions, for which you have received a pay-as-you-earn tax statement, please enter in Anlage N.

(2022): Which pensions must be declared in the tax return?

Next stage for retirement at 67 begins

In 2022, those born in 1957 will turn 65 and reach the previous statutory retirement age of 65. It's time to retire. However, in 2012, the "retirement at 67" began for new retirees, and specific limits must be observed.

Standard retirement age: The standard retirement age has been gradually raised from 65 to 67 since 2012, initially by one month per birth year and from 2024 by two months per birth year. This means that the 1946 birth cohort was the last to retire without deductions at the age of 65 in 2011. Therefore, those who reached the statutory retirement age of 65 in 2012 could only receive their pension without deductions one month later. This was the 1947 birth cohort. For example, someone born on 15/02/1947 would not receive their pension from 01/03/2012 but from 01/04/2012.

The next stage comes into effect on 01/01/2022: Those who turn 65 in 2022 must now work or wait 11 months longer to receive their statutory pension without deductions. This applies to those born in 1957.

Pension for those with particularly long insurance periods: From 01/07/2014, those who can prove at least 45 contribution years may or could receive their pension at 63 without deductions. For those born between 1953 and 1964, the retirement age of 63 is gradually being raised to 65. The increase has been in steps of 2 months per birth year since 2016. In 2022, those born in 1959 will reach the age of 63. Those with 45 insurance years can receive their pension at 63 plus 14 months, i.e., at 64 plus 2 months. Insured persons born on or after 01/01/1964 can only claim the pension without deductions at 65 with 45 contribution years - they no longer benefit from the temporary special regulation.

Pension for those with long insurance periods: Those who can prove 35 contribution years can take the "pension for those with long insurance periods" early at 63 but must accept lifelong deductions. The number of deduction months increases in line with the standard retirement age for those born from 1949 onwards.

In 2022, those born in 1959 can receive their pension at 63 with a lifelong deduction of 11.4%.

Disability pension: The pension for severely disabled people is available to those who are disabled at the start of the pension and have completed the minimum insurance period (waiting period) of 35 years. Those born in 1959 can receive the pension without deductions at 64 plus 2 months. At 61, the pension can be drawn with a deduction of 10.8%. Protection of legitimate expectations: If you were born before 01/01/1964, were disabled on 01/01/2007, and received adjustment payments for dismissed mining employees, you can still retire at 63 without deductions. With a deduction of 10.8%, you can take the pension early at 60 (Source: Deutsche Rentenversicherung, "The right pension for you", 16th edition, 07/2021).

Reduced earning capacity pension: In the case of full reduction in earning capacity, the reduced earning capacity pension can be claimed before the standard retirement age without deductions. In 2022, a reduced earning capacity pension without deductions is paid at 64 plus 8 months. If taken earlier, deductions of 0.3% per month must be accepted, up to a maximum of 10.8%.

Since 01/01/2019, the credit period for reduced earning capacity pensions for new pension entries has been extended earlier and to a greater extent:

- For pensions starting in 2018, the credit period ends at the age of 62 and 3 months under the previous legislation.

- For pensions starting in 2019, the credit period is extended in one step to the age of 65 and 8 months.

- For pensions starting between 2020 and 2031, the credit period is gradually extended to the age of 67, just like the retirement age. The gradual extension begins in 2020 with an increase of one month. The steps of the increase are then one month per calendar year until 2027. From 2028, the credit period is increased by two months per calendar year.

- For pensions starting from 2031, the credit period ends at the age of 67.

From 2031, those with reduced earning capacity will be treated as if they had worked until the standard retirement age, according to the evaluation of their credit period. The credit period ends at the age of 67. The same applies to pensions due to death. The extension is also transferred to the farmers' pension scheme.

The credit period ends at the latest when the standard retirement age is reached. If the deceased insured person was entitled to a reduced earning capacity pension at the time of death, a credit period is only taken into account for a subsequent survivor's pension to the extent that it was credited in the previous reduced earning capacity pension.

Note: The benefit improvements only favour new reduced earning capacity pensions granted from 01/01/2019. They do not apply to those already receiving a reduced earning capacity pension on 01/01/2019. Existing pensions are not recalculated.

Widow's or widower's pension: The age limit for receiving the large widow's or widower's pension is gradually being raised from 45 to 47 between 2012 and 2029. The steps of the increase are initially one month per year from 2012 to 2023 and two months per year from 2024 to 2029.

If the insured person dies in 2022, the age limit for the large widow's or widower's pension is 45 years and 11 months. The large widow's or widower's pension amounts to 60% of the deceased spouse's retirement pension calculated at the time of death. The pension type factor is therefore 0.6. Widows or widowers under 45 years (plus x months) are entitled to a small widow's or widower's pension after the death of the insured spouse. This amounts to 25% of the deceased spouse's retirement pension calculated at the time of death, with a pension type factor of 0.25. Upon reaching the age of 45 plus 10 months, the small pension is converted into a large widow's or widower's pension.

Pension taxation: For pensions starting in 2022, the taxable portion of the pension is 82%. The taxable portion is taxed in the year the pension begins and in the second year of receipt. The remaining amount in the second year is the personal pension allowance, which remains tax-free for life. From the third year, the pension is fully taxable after deducting the personal pension allowance and the standard allowance for income-related expenses of 102 euros.

(2022): Next stage for retirement at 67 begins

Pensioners: Tax exemption for the basic pension supplement

Since 1 January 2021, there has been a basic pension for long-term insurance in the statutory pension scheme. This is not a new type of pension, but merely a supplement to the statutory pension (introduced with the "Act on the Introduction of the Basic Pension for Long-Term Insurance in the Statutory Pension Scheme with Below-Average Income and for Further Measures to Increase Retirement Income" - Basic Pension Act - of 12 August 2020).

- The calculation of the individual basic pension supplement is based on a legally defined calculation method. An income test is carried out to determine the basic pension requirement. If the income exceeds legally defined income allowances, the basic pension supplement is reduced. A basic entitlement to a basic pension supplement may therefore vary in amount in individual years due to the income test.

- The introduction of the basic pension supplement aimed to strengthen confidence in the basic promise of the welfare state to provide security and in the performance of the statutory pension scheme. Against this background, it should also be ensured from a tax perspective that the basic pension supplement, which recognises the lifetime achievement of the entitled person, is not reduced.

Neu

Retroactively from 2021, the portion of the pension paid due to the basic pension supplement is tax-free. This means that the basic pension supplement is fully available without tax deductions and can contribute in full to securing the livelihood (§ 3 No. 14a EStG, inserted by the "Annual Tax Act 2022").

In many cases, a basic pension supplement was already paid in 2021. Consequently, this partial amount was reported as taxable in the pension reference statement for 2021 to the tax authorities. For the retroactive tax exemption, the statutory pension insurance providers are now required to submit corrected pension reference statements to the tax office, showing the amount of the tax-free basic pension supplement.

If an income tax return has already been submitted for 2021 and the tax assessment has even become final, the tax office will now correct it. However, the change will only be made to the extent resulting from the corrected pension reference statement. Other amendment regulations remain unaffected (§ 52 para. 4 sentences 5 to 8 EStG).

(2022): Pensioners: Tax exemption for the basic pension supplement

Which pensions do not need to be declared in the tax return?

Pensions are generally subject to income tax.

However, some types of pensions are completely tax-free and do not need to be declared. These include:

- Pensions from statutory accident insurance (e.g. occupational injury pensions),

- War and disability pensions,

- Monetary pensions paid directly as compensation for suffering under Nazi or GDR injustice.

Compensation pensions for increased needs, loss of maintenance and services, as well as pain and suffering pensions, are not considered income.

(2022): Which pensions do not need to be declared in the tax return?

Which pensions are taxable?

Most pensions are subject to tax. This includes old-age pensions and disability pensions, (large and small) widow's or widower's pensions, orphan's pensions, company pensions (from direct insurance), and pensions from life insurance policies. Different tax rules apply depending on the type of pension.

You do not need to pay tax on a pension received from statutory accident insurance (occupational accident insurance), a war pension, a severe disability pension, a reparation pension, a compensation pension for loss of maintenance under § 844 (2) BGB, a thalidomide pension, a pension for victims of SED injustice, a compensation pension for HIV-infected or AIDS-affected individuals, or a lifelong lottery pension.

(2022): Which pensions are taxable?

Which allowances can pensioners use?

Pensioners who submit an income tax return can enter various allowances and incurred costs to reduce their taxable income.

Personal pension allowance

The pension allowance is determined in the second full year of receiving the pension. In the year the pension begins and in the second year, the pension is taxed at the so-called taxable rate. The remaining amount in the second year is the personal pension allowance, which remains tax-free for life. From the third year, the pension is fully taxable after deducting the personal pension allowance and the standard allowance for income-related expenses of 102 Euro.

Allowance for civil servants and company pensioners

Like the pension allowance, the allowance for civil servants and company pensioners will gradually decrease to zero percent by 2040. This allowance only applies to pensions and company pensions from direct commitments and support funds. In addition, pensioners receive a supplement to the allowance, which also decreases over time.

Here are the figures for pension start in 2022:

For retirement in 2022, the allowance is 14.4% of the pension, up to a maximum of 1.080 Euro, and the supplement is 324 Euro. Together with the standard allowance for income-related expenses of 102 Euro, the pension is tax-free up to 1.506 Euro for life.

Old-age relief amount

The old-age relief amount can be used by pensioners who receive additional income or wages alongside their pension. Additional income includes, for example, income from rental, capital assets, self-employment, private sales transactions, or Riester pensions. However, the tax office first deducts various amounts (saver's allowance, income-related expenses). The amount of the old-age relief depends on the pensioner's year of birth.

If you turned 64 in 2021 (born between 2.1.1957 and 1.1.1958), you will receive an old-age relief amount from 2022 for life of 14.4% of the income, up to a maximum of 684 Euro.

If you turn 64 in 2022 (born between 2.1.1958 and 1.1.1959), the old-age relief amount from 2023 is 13.6%, up to a maximum of 646 Euro.

Standard allowance for income-related expenses

For the pension, every taxpayer receives a standard allowance for income-related expenses of 102 Euro per year.

Special expenses

Contributions to statutory health and long-term care insurance can also be entered by pensioners as special expenses in the "Anlage Vorsorgeaufwand". Pensioners receive a health insurance subsidy from their pension insurance provider, which must be deducted from the contributions. Donations can be deducted as special expenses for tax purposes. The collected donation receipts thus reduce the taxable income. If you do not donate or have no other special expenses, the tax office deducts a flat rate of 36 Euro.

Exceptional expenses

Especially for older and sick people, exceptional expenses can arise that reduce taxable income. This could be accommodation in a nursing home, employing a household help, or hiring a tradesperson. But also medical costs, such as medication, glasses, or dental prostheses, can be claimed by pensioners.

Mini job

If a pensioner (over 65 years) takes on a mini job, this income is tax-free for them.

Tip

If, as a pensioner, you remain below the tax-free allowance of 10.347 Euro (2022) with the various allowances, flat rates, and deductible costs, you do not have to pay any tax on your income. For married couples, the amount is doubled.

(2022): Which allowances can pensioners use?