What new benefits are there for the disability pension?

If you can no longer work or can only work to a limited extent due to a chronic illness or accident, you may receive a disability pension from the statutory pension insurance under certain conditions. If the pension was approved before 1 July 2014, it was calculated as if the person concerned had been employed until the age of 60 with their previous average income (so-called credit period according to § 59 SGB VI).

On 1 July 2014, there were two positive changes for early retirees:

(1) For disability pensions approved since 1 July 2014, the credit period has been extended from age 60 to age 62. The pension is therefore calculated as if the person had worked until the age of 62. This results in a slightly higher pension.

(2) In addition to the length of the credit period, the amount of earnings is also important for the disability pension. Previously, the credit period was valued at the average income. Since 1 July 2014, the last four years before the onset of the disability are no longer taken into account if the salary had already decreased for health reasons during this period. Due to the new regulation, the elimination of overtime or the switch to part-time work no longer has a negative impact on the pension.

Important

Unfortunately, people who were already receiving a disability pension on 1 July 2014 do not benefit from the improved disability pension. Existing pensions are not recalculated. The new regulation only applies to disability pensions newly approved from 1 July 2014. The deductions for disability pensions of up to 10.8% remain unchanged.

From 1 January 2018, the credit period for the disability pension for new pension approvals has been gradually extended from age 62 to age 65 (§ 59 SGB VI).

- For pensions starting in 2018, the credit period ends at the age of 62 years and 3 months according to the previous legal situation.

- For pensions starting in 2019, the credit period is extended in one step to the age of 65 years and 8 months.

- For pensions starting between 2020 and 2031, the credit period - like the retirement age - is gradually extended to the age of 67. The gradual extension begins in 2020 with an increase of one month. The increase steps are then also one month per calendar year until 2027. From 2028, the credit period is increased by two months per calendar year.

- For pensions starting from 2031, the credit period ends at the age of 67.

(2022): What new benefits are there for the disability pension?

What is a statutory annuity?

Annuities are fixed payments linked to a person's lifetime. Annuities and other benefits from statutory pension insurance, the agricultural pension fund, and professional pension schemes are only partially taxable, depending on the year the pension started.

If you have received a pension from statutory pension insurance, you can request a “Statement for submission to the tax office” regarding your pension income as a filling aid. This will then be sent to you automatically in subsequent years. If the pension started in 2020, the taxable portion is 80%.

No entries regarding the taxable portion are required in the tax return. The tax-free part of the pension is determined in the year following the start of the pension and generally applies for the entire duration of the pension. In subsequent years, this amount is deducted from the annual (gross) pension amount.

Pension increases based on regular adjustments are fully taxable. The same applies to benefits from private basic pension contracts (so-called Rürup pensions).

Annuities include in particular

- old-age pensions,

- disability pensions,

- incapacity pensions,

- occupational disability pensions,

- survivor's pensions such as widow's/widower's pensions,

- orphan's pensions, or

- parental pensions.

One-off payments, such as death benefits or settlements of small pensions, must also be declared. If you have been recognised as a victim of National Socialist persecution under § 1 of the Federal Compensation Act (BEG) and pension periods due to persecution were taken into account in the calculation of your statutory pension, please inform the tax office informally.

Such periods may have been considered under the Act on the Payment of Pensions from Employment in a Ghetto (ZRBG), the Act on the Settlement of National Socialist Injustice in Social Insurance (WGSVG), or the Foreign Pensions Act (FRG). This also applies to widow's/widower's pensions if the deceased was recognised as a victim under § 1 BEG and the pension includes corresponding pension periods. The tax office will check whether this pension is tax-free.

(2022): What is a statutory annuity?

Which income-related expenses can I claim as a pensioner?

Even as a pensioner, you can claim expenses related to your pension as income-related expenses in your tax return. If your income-related expenses total less than 102 Euro, it is not worth entering them. The tax office automatically applies an income-related expenses allowance of 102 Euro, which is immediately deducted from your income. This allowance is applied jointly for all pensions and all income that must be declared under other income. It is an annual amount that is not reduced, even if the conditions did not apply for the entire year or if there was no income for the whole year. The income-related expenses allowance is personal and is available to each spouse separately as soon as they have the relevant income.

Tip: If you have higher expenses exceeding the allowance of 102 Euro, it is definitely worth entering them. However, you should also have the evidence ready and enclose it with your tax return. If you have expenses for a tax advisor, the tax office will only recognise the costs as income-related expenses if they are related to your pension. Therefore, ask your tax advisor to specify separately in their invoice the part that directly relates to your pension.

Income-related expenses you can claim include, for example, expenses for a

- pension advisor,

- lawyer in pension disputes,

- tax advisor (only for form R), and also

- costs related to applying for a pension (travel expenses, office supplies, postage, telephone costs)

- court fees if the case concerns your pension

- union fees you pay as a pensioner

- flat-rate account maintenance fee of 16 Euro per year

Tip

If you are unsure whether the tax office will recognise a particular expense, simply declare it and enclose the evidence. The tax officer will decide.

(2022): Which income-related expenses can I claim as a pensioner?

What does the 2005 Retirement Income Act regulate?

The Pension Income Act regulates the taxation of pensions. It affects everyone, both pensioners who were already retired in 2005 and all future retirees. The tax burden for new pensioners increases year by year - at the same time, the benefits for employees also grow.

Tax-advantaged pension provision

In addition to the statutory pension insurance, private pension insurance is also recognised as a pension provision (so-called basic pension or Rürup pension). Contributions to private pension insurance are only tax-advantaged if the insurance is aimed at a lifelong pension for the taxpayer. In addition, the insured person must be at least 60 years old when the pension payments begin. For contracts concluded from 2012 onwards, pension payments may not begin until the age of 62. This ensures that they are pension provision products. Furthermore, pension entitlements must not be transferable, pledgeable, sellable, or capitalisable. The insurance sum must also be paid out as an annuity; lump-sum payments are generally prohibited. However, tax-advantaged pension products can be supplemented with additional insurance - for example, occupational disability insurance.

Investment products that do not necessarily serve as pension provision are not tax-advantaged. These are usually freely available capital investments, which also include endowment life insurance. An exception is endowment life insurance policies concluded before 2005. They remain tax-free.

For pensioners, this means the following:

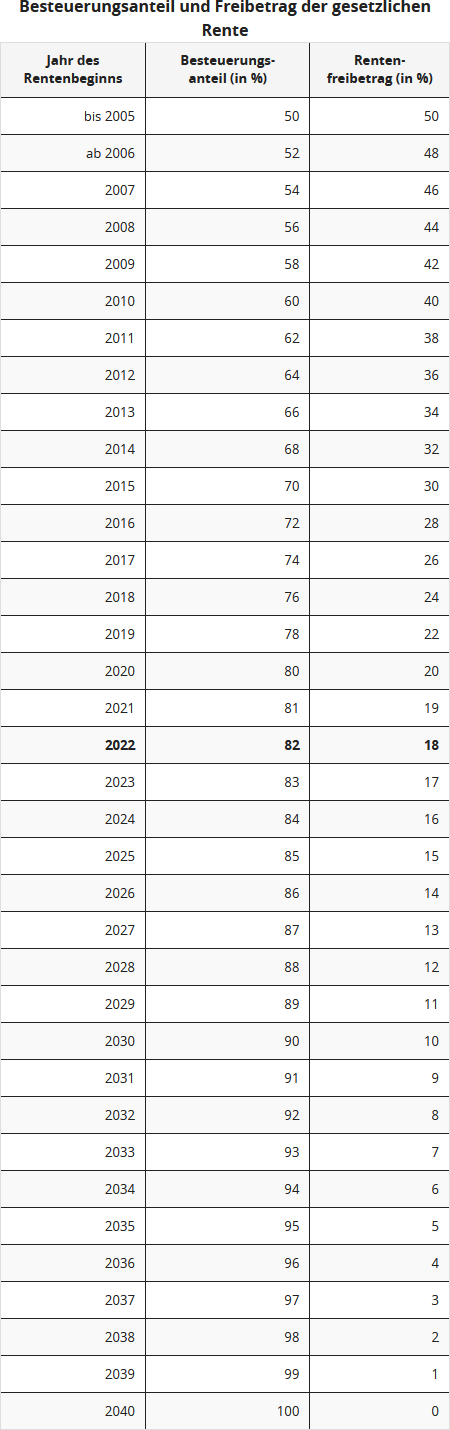

Since 2005, 50 per cent of pension income has been taxable. From 2006 to 2020, the taxable portion of pensions increases by two percentage points annually, and from 2021, the portion increases by only one percentage point per year. In 2040, the pension will be 100 per cent taxable, whereas employee contributions to pension provision will then be largely tax-free.

Also regulated in the Pension Income Act: Temporary pensions, such as disability pensions, and non-temporary pensions, such as old-age pensions, have been treated equally for tax purposes since 2005. Pensions from insurance policies that are tax-advantaged during the accumulation phase are taxable during the payout phase.

Note:

At the end of May 2021, the Federal Fiscal Court published its two rulings on the possible double taxation of pensions. However, the lawsuits filed by the affected pensioners were unsuccessful. The Federal Fiscal Court considers double taxation to be possible only in a few individual cases. It considers the basic system of pension taxation to be lawful, i.e. the limited deduction of pension expenses during working life, combined with the partial tax exemption of pensions during the payout phase. Double taxation is only likely to occur for later generations of pensioners (Federal Fiscal Court rulings of 19.5.2021, X R 33/19 and X R 20/21). However, the unsuccessful plaintiffs have lodged a constitutional complaint against the two decisions of the Federal Fiscal Court (Ref. 2 BvR 1143/21 and 2 BvR 1140/21).

The issue is how double taxation is calculated in detail. The Federal Fiscal Court has taken a very schematic view, which only leads to excessive taxation of pensions in individual cases. For the calculation of possible double taxation, the nominal value principle applies. In simple terms, the actual contributions paid and subsidised pension expenses are to be compared with the actual pension payments received, which are partially exempt. Neither amounts are to be discounted or compounded, nor is inflation to be taken into account.

However, some experts, as well as the plaintiffs in case X R 33/19, argued that during the working phase, no pension amounts are acquired in cash, but rather pure pension points. The actual amount of the pension only becomes clear much later. However, the Federal Fiscal Court did not delve into the "depths" of financial and insurance mathematics but compared contributions paid with payments received. Whether this is correct or whether there is a more favourable calculation for taxpayers is to be clarified by the constitutional judges in Karlsruhe.

The federal and state governments have now finally agreed to issue affected tax assessments on a provisional basis regarding the disputed point. Specifically, tax assessments are issued provisionally with regard to the "taxation of annuities and other benefits from basic provision under section 22 number 1 sentence 3 letter a double letter aa EStG". The provisional note is attached to all income tax assessments for assessment periods from 2005 onwards in which an annuity or other benefit from the so-called basic provision is recorded (BMF letter of 30.8.2021, V A 3 - S 0338/19/10006 :001).

This means that pensioners will now receive income tax assessments with a note on the - partial - provisional nature of the tax assessment. If the Federal Constitutional Court finds that the current taxation of statutory pensions and pensions from occupational pension schemes and similar pension schemes is unconstitutionally high, the tax assessments issued now and in the future can be amended without a prior objection.

(2022): What does the 2005 Retirement Income Act regulate?

How is the statutory pension taxed?

The legislator reformed the taxation of state pensions in 2005 with the Retirement Income Act. Since then, a fixed portion of the pension is taxable, while the rest remains (for now) tax-free. You must pay tax on your pension income; this is known as deferred taxation. The amount you need to tax depends on the year you started receiving your pension.

For individuals who retired in 2005 or earlier, the tax-free portion was 50 per cent. A (personal) allowance is created from the non-taxable pension, allowing these pensioners to use a "pension allowance" of 50 per cent from 2005 onwards. This pension allowance remains unchanged for life.

Since 2005, the so-called taxable portion has increased annually by two percentage points, and from 2021 by one percentage point per year. Thus, individuals retiring from 2040 onwards will have to fully tax their state pension income.

The tax office automatically deducts an allowance for advertising costs of 102 Euro without further proof. If you have higher expenses, you should declare them in your tax return to reduce your taxable income. You can declare, for example, tax consultancy costs (for form R), pension advice, or a lawyer if they support you with pension matters. However, you must prove the higher expenses in any case.

Example

Hans Müller retired on 1 January 2009 and received a state pension of 12.000 Euro last year. For Hans Müller, 58 per cent of his pension is taxable, and the pension allowance is 42 per cent. Thus, Müller would have to declare 6.960 Euro as income to the tax office for the year. However, if he has no other income, he does not have to submit a tax return, as the amount is below the basic allowance of 10.347 Euro (2022).

The lifelong pension allowance for Hans Müller is 5.040 Euro. However, he would only have to tax income above this allowance if it also exceeds the basic allowance.

Income from renting and leasing or capital gains must, however, be added to the income.

If Hans Müller were to receive a pension of 15.000 Euro and retire in 2022, he would have to tax 12.300 Euro (82 per cent) of his pension and therefore also submit a tax return.

Note: The pension allowance for Müller remains the same for life. Even if his pension income increases due to pension adjustments, only 5.040 Euro would be tax-free each year in the first example. The allowance refers to a specific amount of money, not a percentage of the respective pension. Thus, Mr Müller must fully tax future pension adjustments.

(2022): How is the statutory pension taxed?

What does the opening clause mean?

With deferred taxation, there can be unfair over-taxation if a self-employed person has paid contributions to an occupational pension scheme over several years that were higher than the annual maximum contribution in the statutory pension insurance (sum of employer's and employee's share). The maximum amount to be paid is based on the contribution assessment ceiling.

This is recalculated annually and represents the limit up to which pension insurance contributions must be paid as a proportion of income. For income above the contribution assessment ceiling, you usually do not pay insurance contributions – unless you pay them voluntarily as in this context.

The self-employed person has therefore voluntarily paid additional contributions from their already taxed income. As a result, they have earned a higher pension, but on the other hand, they would have to tax it too highly with the usual tax rate. This can be avoided. As a pensioner, they can have their pension divided into a voluntary and a statutory part. However, they must have paid a higher voluntary contribution for at least ten years by 31.12.2004.

Tip

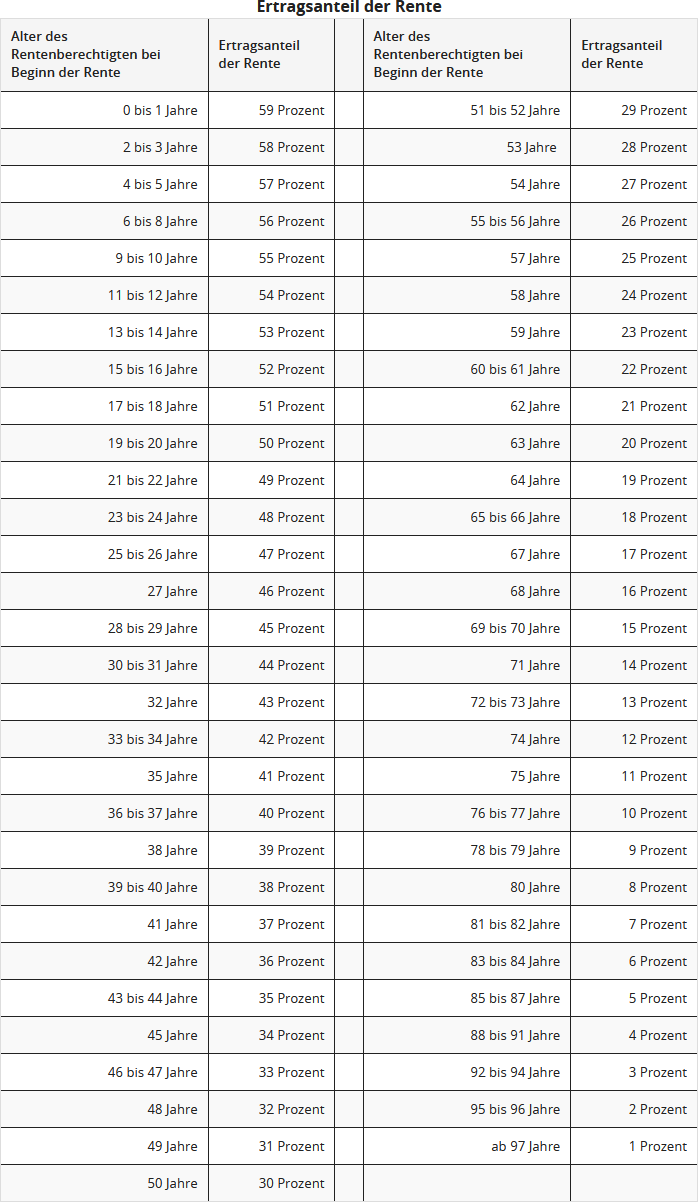

If this applies to you, you must apply for the portion of your pension based on these increased contributions to be taxed not at the high tax rate (2022: 82 percent of the pension) but at the significantly more favourable income share. The portion of the pension to be taxed at a lower rate is the opening clause, which you can find in the certificate from your pension insurance provider.

Example

If you have been receiving a statutory pension of 1.500 Euro per month since the age of 65 and can prove to the tax office with a certificate from the pension payment office that 30 percent (this is the opening clause) of the pension payment is based on increased contributions, the following calculation applies:

For 70 percent of the pension: Normal taxation after deduction of the pension allowance: 1.500 Euro x 70 percent = 1.050 Euro x 12 months = 12.600 Euro minus pension allowance of (for example) 42 percent = 7.308 Euro.

For the part for which the opening clause of 30 percent applies, the more favourable income share is applied: 1.500 Euro x 30 percent = 450 Euro x 12 months = 5.400 Euro x 18 percent = 972 Euro. In this case, 8.280 Euro would have to be taxed. Without the opening clause, 10.440 Euro would have had to be taxed.

The income share depends on the age of the pensioner at the start of the pension payment, for example, it is 19 percent for 64-year-olds, 18 percent for 65 to 66-year-olds, and 17 percent for 67-year-olds.

The following table shows the amount of the income share depending on the age at the start of the pension; this is automatically calculated by Lohnsteuer kompakt:

Note:

At the end of May 2021, the Federal Fiscal Court published its two rulings on the possible double taxation of pensions. However, the claims of the affected pensioners were unsuccessful. The BFH considers double taxation to be possible only in a few individual cases. It considers the basic system of pension taxation to be lawful, i.e. the limited deduction of pension expenses during working life, combined with the partial tax exemption of pensions during the payout phase. Double taxation is only expected for later pension cohorts (BFH rulings of 19.5.2021, X R 33/19 and X R 20/21). However, the unsuccessful plaintiffs have lodged a constitutional complaint against the two BFH decisions (Ref. 2 BvR 1143/21 and 2 BvR 1140/21).

The issue is how double taxation is calculated in detail. The BFH has taken a very schematic view, which only leads to excessive taxation of pensions in individual cases. For the calculation of possible double taxation, the nominal value principle applies. In simple terms, the actual contributions paid and benefited from must be compared with the actual pension payments received and partially exempted. Neither amounts are to be discounted nor is inflation to be taken into account.

However, some experts, as well as the plaintiffs in case X R 33/19, argued that during the working phase, no pension amounts are acquired in cash, but rather pure pension points. The actual amount of the pension only becomes clear much later. But the BFH did not delve into the "depths" of financial and insurance mathematics, but rather compares amounts paid in with amounts paid out. Whether this is correct or whether there is a more favourable calculation for taxpayers is to be clarified by the constitutional judges in Karlsruhe.

Currently, the federal and state governments have finally been able to agree to issue affected tax assessments on a provisional basis regarding the disputed point. Specifically, tax assessments are issued provisionally regarding the "taxation of annuities and other benefits from basic provision under § 22 number 1 sentence 3 letter a double letter aa EStG". The provisional note is attached to all income tax assessments for assessment periods from 2005 in which an annuity or other benefit from the so-called basic provision is recorded (BMF letter of 30.8.2021, V A 3 - S 0338/19/10006 :001).

This means that pensioners will now receive income tax assessments with a note on the - partial - provisional nature of the tax assessment. If the Federal Constitutional Court finds that the current taxation of statutory pensions and pensions from occupational pension schemes and similar pension schemes is unconstitutionally high, the tax assessments issued now and in the future can be changed without a prior objection.

(2022): What does the opening clause mean?

What should I enter for the pension adjustment?

For pension adjustments, you must specify the difference between your current monthly pension and your pension from the year in which the pension allowance was set. This tax allowance is set in the year following the start of your pension. The pension allowance is valid for life. You can find the pension adjustment on the pension adjustment notice or ask your pension provider or insurance company. This means that all future pension increases are fully taxable, as the allowance remains unchanged despite the increases.

If you retired in 2013, the pension allowance was fixed for you in 2014.

Example: The pension adjustment is the difference between the pension payments from 2013 and 2021. If pensions are adjusted, this usually happens on 1 July of a year.

Pension payments 2014: 6 x 1.050 Euro + 6 x 1.056 Euro = 12.636 Euro

Pension payments 2021: 6 x 1.380 Euro + 6 x 1.420 Euro = 16.800 Euro

=> Pension adjustment = 4.164 Euro

To determine the pension adjustment for 2022, subtract the pension payments you received in the second pension year from your 2022 pension payments.

Tip

Irregular changes in the pension amount, for example because other income was credited to you or this income was temporarily discontinued, are not part of the pension adjustment.

(2022): What should I enter for the pension adjustment?

How is interest on pension arrears treated?

Pensions are often approved at a later date and then paid retroactively in a lump sum, for example, due to legal disputes or after clarification of the facts. The insurance provider must pay additional interest on a pension back payment - in the case of pensions from the statutory pension insurance, this is 4% p.a. (§ 44 Abs. 1 SGB I).

This back payment interest is taxable as "income from capital assets" (BFH ruling of 9.6.2015, VIII R 18/12; also BMF letter of 4.7.2016, IV C 3-S 2255/15/10001).

Previously, the tax authorities treated the back payment interest as "other income" and taxed it, like the pensions and pension back payments of the basic provision (statutory pension, Rürup pension, pension from an occupational pension scheme), with the taxable portion as "other income". The taxable portion is determined by the year the annuity begins, e.g. in 2015 with 70%.

Tip

The new BFH ruling means that the interest on the pension back payment is now fully taxable as capital income, but remains tax-free within the saver’s allowance of 801 Euro or 1.602 Euro. Since the pension insurance provider does not withhold withholding tax, you must declare the interest in the "Anlage KAP" as part of your tax return.

Unlike before, you may no longer enter the interest in the "Anlage R". The pension back payment itself is tax-advantaged according to the one-fifth rule (in accordance with § 34 EStG).

(2022): How is interest on pension arrears treated?

How is my pension from an occupational pension scheme taxed?

Pensions from occupational pension schemes are part of the so-called basic provision, like pensions from the statutory pension insurance. This means:

- Taxation is based on the so-called taxable portion. This is a certain percentage legally fixed for the year the pension begins.

- This taxable portion depends on the year the pension begins. It starts at 50 per cent in 2005 and increases by 2 percentage points for each new pensioner cohort from 2006 to 2020, and by 1 percentage point from 2021 to 2040.

- The taxable portion is applied only in the year the pension begins and in the second year of receiving the pension.

- In the second year of receiving the pension, the remaining amount after deducting the taxable portion is the personal pension allowance, which remains tax-free for life.

- From the third year onwards, the full pension amount is taxable after deducting the personal pension allowance and the standard allowance for income-related expenses of 102 Euro.

- Since the pension allowance remains unchanged for life, any pension increase is fully taxable.

The tax office automatically deducts a standard allowance for income-related expenses of 102 Euro without further proof. If you have higher expenses, you should declare them in your tax return to reduce your taxable income.

You can declare, for example, tax consultancy costs (for form R), pension advice, or a lawyer if they support you with pension matters. However, you must prove these higher expenses.

Example

Hans Müller retired on 1 January 2009 and received a pension of 12.000 Euro last year. For Hans Müller, 58 per cent of his pension is taxable, and the pension allowance is 42 per cent. So, Müller would have to declare 6.960 Euro as income to the tax office for the year.

However, if he has no other income, he does not have to submit a tax return, as the amount is below the basic allowance of 10.347 Euro (2022). Hans Müller's lifelong pension allowance is 5.040 Euro. Income above this allowance would only be taxable if it also exceeds the basic allowance.

However: Income from renting and leasing or capital gains must be added to the income.

If Hans Müller were to receive a pension of 15.000 Euro and retire in 2022, he would have to tax 12.300 Euro (82 per cent) of his pension and therefore also submit a tax return.

Note: The pension allowance for Müller remains the same for life. Even if his income from the pension increases after pension adjustments, only 5.040 Euro would be tax-free each year in the first example. The allowance refers to a specific amount, not a percentage of the respective pension. Thus, Mr Müller must fully tax future pension adjustments.

(2022): How is my pension from an occupational pension scheme taxed?

How is my pension from an agricultural pension fund taxed?

Pensions from agricultural pension funds, like pensions from the statutory pension insurance, are part of the so-called basic provision. This means:

- Taxation is based on the so-called taxable portion. This is a certain percentage legally fixed for the year the pension begins.

- This taxable portion depends on the year the pension begins. It starts at 50 per cent in 2005 and increases by 2 percentage points for each new pensioner cohort from 2006 to 2020, and by 1 percentage point from 2021 to 2040.

- The taxable portion is applied only in the year the pension begins and in the second year of receiving the pension.

- In the second year of receiving the pension, the remaining amount after deducting the taxable portion is the personal pension allowance, which remains tax-free for life.

- From the third year onwards, the pension is fully taxable after deducting the personal pension allowance and the standard allowance for income-related expenses of 102 Euro.

- Since the pension allowance remains unchanged for life, any pension increase is fully taxable.

Example

Hans Müller retired on 1 January 2009 and received a statutory pension of 12.000 Euro last year. For Hans Müller, 58 per cent of his pension is taxable, and the pension allowance is 42 per cent.

Thus, Müller would have to declare 6.960 Euro as income to the tax office for the year. However, if he has no other income, he does not have to submit a tax return, as the amount is below the basic allowance of 10.347 Euro (2022).

The lifelong pension allowance for Hans Müller is 5.040 Euro. He would only have to pay tax on income above this allowance if it exceeds the basic allowance.

However: Income from renting and leasing or capital gains must be added to the income.

If Hans Müller were to receive a pension of 15.000 Euro and retire in 2022, he would have to pay tax on 12.300 Euro (82 per cent) of his pension and therefore also submit a tax return.

Note: The pension allowance for Müller remains the same for the rest of his life. Even if his income from the pension increases after pension adjustments, only 5.040 Euro would be tax-free each year in the first example. The allowance refers to a specific amount of money, not a percentage of the respective pension. Thus, Mr Müller must fully tax future pension adjustments.

The tax office automatically deducts a standard allowance for income-related expenses of 102 Euro without further proof. If you have higher expenses, you should declare them in your tax return to reduce your taxable income. You can declare, for example, tax consultancy costs (for form R), pension advice, or a lawyer if they support you with pension matters. However, you must provide evidence of these higher expenses.

(2022): How is my pension from an agricultural pension fund taxed?

How is the mother's pension taxed?

In July 2014, the child-rearing period for pensioners with children born before 1992 was extended from 12 to 24 months. Instead of one earnings point, two earnings points are now granted as a supplement to the current pension. This means a pension increase of 28.61 Euro (West) or 26.39 Euro (East) per child. How is this pension increase, known as the "Mütterrente", taxed?

- In November 2014, a decree from the Ministry of Finance of Schleswig-Holstein provided - supposed - clarity: The pension increase due to additional child-rearing periods is not considered a regular pension adjustment but an extraordinary re-determination of the annual pension amount. Therefore, the tax-free portion of the pension must be recalculated, and the previous pension allowance increased to raise the tax-free portion of the "Mütterrente" (Ministry of Finance Schleswig-Holstein, 10.11.2014, VI 307-S 2255-152).

- The officials from Schleswig-Holstein also provided an example: For a pensioner whose pension began before 2005, the taxable portion - as it was then for the old-age pension - is also 50% for the additional "Mütterrente", i.e., 50% of the pension paid! If the pension began in 2007, the taxable portion is 54%, and the pension allowance is 46%; if the pension began in 2010, the taxable portion is 60%, and the pension allowance is 40%, etc. Finally, a simple solution. This is how PC programs have calculated so far.

- But it would be surprising if the tax authorities did not find a way to make the calculation more complicated and take more money from pension mothers. Indeed, the tax assessments for 2014 unexpectedly show a higher tax share of the pension than previously assumed.

Currently, the Federal Ministry of Finance points out that the increase in the pension allowance is determined not only based on the taxable portion from the year of the original pension start but also on the pension value from which the previous pension allowance was calculated. The relevant year was the year following the pension start.

Since the pension value usually changes on 1st July of the year, an average pension value must be determined for the relevant following year. The taxable portion at that time is then applied to this value. The value ratios in the year of the initial determination of the pension allowance are decisive, and this is the year following the pension start (BMF, 23.7.2015).

This means that those who have been receiving a pension since 2005 or earlier receive the "Mütterrente" with only 50% of the pension value at that time tax-free. The fictitious increases in the Mütterrente from 2005 to 2014 are treated as pension adjustment amounts and are fully taxable.

Example

Mrs Maier, who retired in 2007, receives a Mütterrente for one child from 1.7.2014 (1 earnings point x current pension value (West) = 28.61 Euro). Her pension thus increases by a total of 171.66 Euro in 2014 (6 x 28.61 Euro). For the taxable portion, the year 2007 is relevant, and for the pension allowance, the value ratios of 2008 are relevant, so a taxable portion of 54% applies, and the remaining 46% are tax-free.

In 2008, the pension value (West) was 26.27 Euro until 30.6. and 26.56 Euro from 1.7., averaging 26.42 Euro rounded up. Since the average pension value (West) in 2008 was 26.42 Euro, this leads to an increase in the pension allowance of 72.92 Euro ([6 x 26.42 Euro] x 46% tax-free portion). Previously, a pension allowance of 78.96 Euro was assumed (46% of 171.66 Euro).

In 2015, the Mütterrente for one child is 346.92 Euro (6 x 28.61 Euro + 6 x 29.21 Euro), and the pension allowance is 145.84 Euro (12 x 26.42 Euro x 46%).

Currently, with the "RV Performance Improvement and Stabilisation Act" since 1.1.2019, the child-rearing period for mothers and fathers whose children were born before 1992 has been further improved and extended from 24 months to 30 months. Instead of 2 earnings points, 2.5 earnings points are now credited to the pension account or granted as a supplement to the current pension, known as "Mütterrente II".

According to the new regulation, the following applies:

◦ For mothers and fathers who retire from 1.1.2019, the child-rearing period is extended by a further 6 months, or the pension entitlement is increased by 0.5 earnings points. Half an earnings point currently corresponds to around 16 Euro (West) and 15.35 Euro (East) per month.

◦ Mothers and fathers who are already receiving a pension at this time will receive a supplement equivalent to the pension yield of half a child-rearing year from 1.1.2019.

◦ Mothers and fathers for whom a supplement for child-rearing from the extension of the child-rearing period in 2014 is already included in the pension will receive a supplement increased by half a personal earnings point in the future, provided they raised the child in the 24th calendar month after the birth month. The regulation essentially corresponds to the regulation that took place in 2014 with the extension of the child-rearing periods to two years. This flat-rate crediting method is carried out, as was the extension of the child-rearing period in 2014, for reasons of administrative simplification so that the pension insurance institutions do not have to reassess millions of pensions (§ 307d para. 1 SGB VI).

◦ From 1.1.2019, those who did not receive a supplement in 2014 (because they did not have a child-rearing period in the pension insurance account in the 12th calendar month) but meet the specified requirements will also receive a supplement of personal earnings points.

◦ In deviation from the regulations made in 2014 when the child-rearing periods were extended, a special right to apply is now intended to provide relief for cases that have not received a supplement of personal earnings points for child-rearing since 1.7.2014 or do not receive a supplement of personal earnings points with the current extension of the crediting of child-rearing periods because it is based on child-rearing in a specific calendar month (child-rearing in the 12th or 24th calendar month). The new right to apply concerns, for example, adoptions or upbringing in Germany after returning from abroad if the adoption or change of residence took place after the 12th or 24th calendar month after the month of birth. However, the prerequisite for recognition is that child-rearing periods or supplements are not already credited to other insured persons or survivors for the same child, as far as this is actually known to the pension insurance institution (§ 307d para. 5 SGB VI).

◦ Also, for mothers born before 1.1.1921 who receive a child-rearing benefit under § 294 SGB VI instead of child-rearing periods, this benefit is increased by the value of half a personal earnings point. This corresponds to the pension yield from the extension of the child-rearing period by half a year (§ 295 SGB VI).

Tip

You do not need to submit a special application to receive the improved benefit. The revaluation of the periods for children born before 1992 is carried out ex officio and does not need to be applied for.

(2022): How is the mother's pension taxed?

Sichern Sie sich einfach die volle Steuererstattung, die Ihnen zusteht!

Nur Lohnsteuer kompakt bietet Ihnen:

- Persönliche Steuertipps im Wert von 312 Euro (Durchschnitt)

- Verständliche Eingabehilfen und Erklärungen

- Import aus jeder beliebigen anderen Steuersoftware

- Schnelle Antworten bei Fragen

Jetzt kostenlos testen