Field help

Enter the amount of expenses incurred for your relocation.

You can claim relocation costs as income-related expenses if you have moved for professional reasons. Occupational reasons exist when you take up your first job or change an employer. In the case of relocations within the same municipality, there is a professional reason, among other things, if the relocation is requested by the employer (e.g. moving into or leaving a company flat).

If your relocation is job-related, you can claim the following costs as income-related expenses:

- Costs for a moving company

- Costs of packing material such as moving boxes, clothes boxes, protective cover

- Rental costs of a transporter or use of your own vehicle/trailer

- Repair costs of damaged removal goods

- Replacement costs of destroyed/lost items

- Fees for no stopping signs

- Travel expenses on the day of the move or for viewing the flat

- Costs of double rental payments/additional rental costs

- Costs of newspaper advertisements and brokerage fees

- Purchasing costs of a stove and heaters

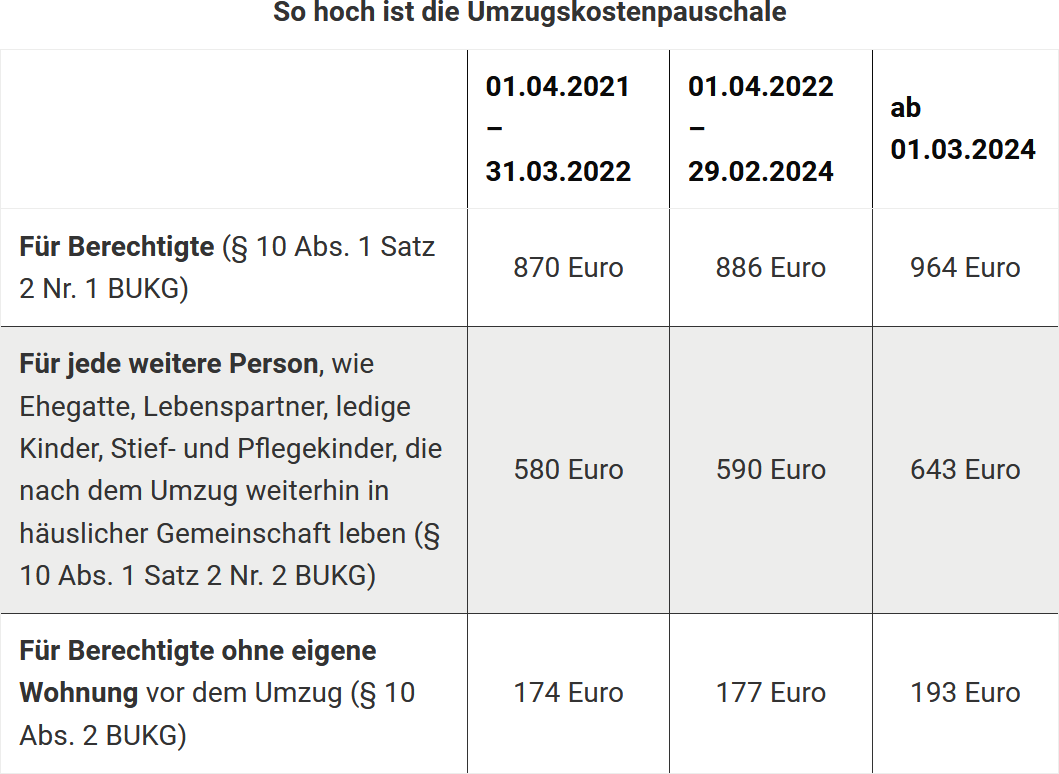

in addition, relocation costs (flat-rate amount for other relocation expenses):

- in case of relocation in 2024:

- 886 Euro for entitled persons,

- 580 Euro for each further household member,

- 177 Euro for beneficiaries who did not have their own flat before relocation.

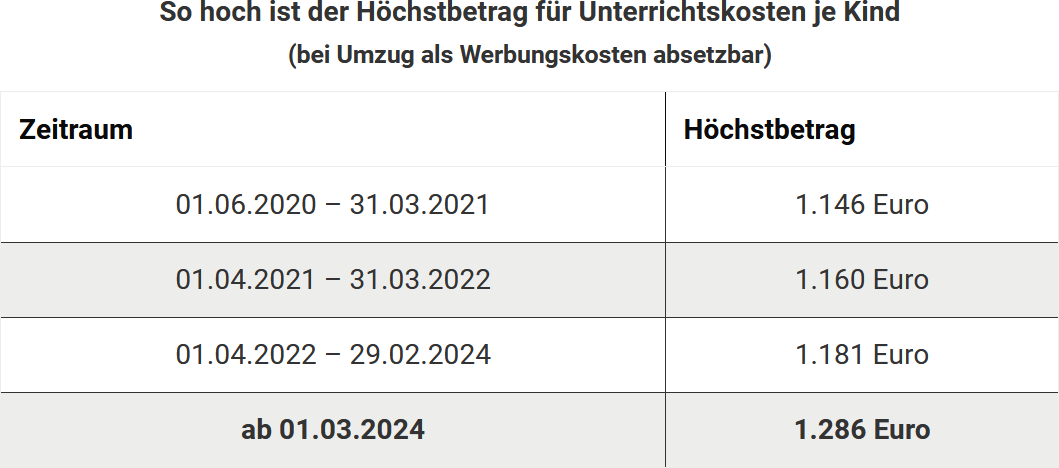

and costs of the children's additional tuition due to the relocation:

- in case of relocation in 2024: a maximum of 1.181 Euro.

Specify which expenses were incurred in the course of the relocation.

You can claim relocation costs as income-related expenses if you have moved for professional reasons. Occupational reasons exist when you take up your first job or change an employer. In the case of relocations within the same municipality, there is a professional reason, among other things, if the relocation is requested by the employer (e.g. moving into or leaving a company flat).

If your relocation is job-related, you can claim the following costs as income-related expenses:

- Costs for a moving company

- Costs of packing material such as moving boxes, clothes boxes, protective cover

- Rental costs of a transporter or use of your own vehicle/trailer

- Repair costs of damaged removal goods

- Replacement costs of destroyed/lost items

- Fees for no stopping signs

- Travel expenses on the day of the move or for viewing the flat

- Costs of double rental payments/additional rental costs

- Costs of newspaper advertisements and brokerage fees

- Purchasing costs of a stove and heaters

in addition, relocation costs (flat-rate amount for other relocation expenses):

- in case of relocation in 2024:

- 886 Euro for entitled persons,

- 590 Euro for each further household member,

- 177 Euro for beneficiaries who did not have their own flat before relocation.

and costs of the children's additional tuition due to the relocation:

- in case of relocation in 2024: a maximum of 1.181 Euro.

If you have incurred travel expenses as part of a work-related relocation, you can claim them in your tax return as income-related expenses.