Caution: Household services are not always deductible

Costs that you have already declared as income-related expenses, business expenses, special expenses, or extraordinary expenses in your tax return cannot also be deducted as household-related services.

You cannot choose how to deduct the costs. If the costs are considered income-related expenses or special expenses, they must be declared as such, the same applies to extraordinary expenses. This applies, for example, to childcare costs, which cannot be deducted as household-related services, even if the maximum amount for childcare costs has already been exceeded.

Also, personal services, such as for a hairdresser or cosmetic treatment, are not considered household-related services, even if they take place in your home.

Services listed in the care insurance service catalogue can, however, be declared.

Not eligible are works carried out outside your private household, for example, if you take your laundry to a dry cleaner.

Craftsman services for which you receive insurance benefits (e.g., household or building insurance) cannot be claimed in the tax return. Insurance benefits that you will receive later must also be included.

There is also no tax deduction for household-related services that do not take place in your private household. This includes, for example, the cleaning of an off-site office, a second home, or your company. Such expenses are considered business expenses or income-related expenses. However, costs for a cleaning help who works both in a home office and in your private home can be proportionately divided. The business part is considered business expenses or income-related expenses, the private part as household-related services.

If household-related services are carried out both on private property and on public land, this activity is entirely tax-favoured according to a BFH ruling. This applies, for example, to snow clearing on public pavements, but not on public roads. The costs for winter service in front of your own property are therefore deductible at 20 percent from the tax liability (BFH ruling of 20.3.2014, VI R 55/12).

However, in 2020, the BFH ruled that expenses for street cleaning in front of the property are not tax-favoured as household-related services according to § 35a para. 2 sentence 1 EStG (BFH ruling of 13.5.2020, VI R 4/18).

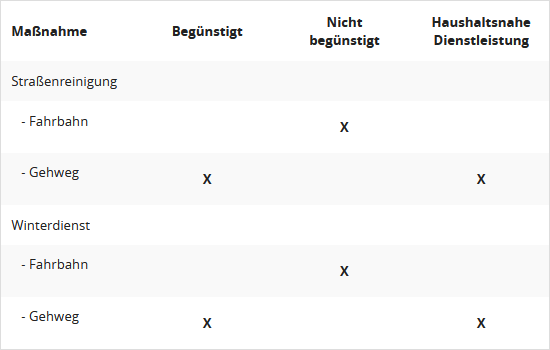

Recently, the Federal Ministry of Finance published the following overview regarding the BFH's case law (BMF letter of 1.9.2021, IV C 8 - S 2296-b/21/10002 :001):

| Measure

|

Eligible

|

Not eligible

|

Household-related service

|

| Street cleaning |

|

|

|

| – Roadway |

|

X |

|

| – Pavement |

X |

|

X |

| Winter service |

|

|

|

| – Roadway |

|

X |

|

| – Pavement |

X |

|

X |

Furthermore, the BMF states: For craftsman services provided by public authorities that benefit not only individual households but all households involved in the public measures, a benefit under § 35a EStG is excluded. There is no spatial-functional connection between the craftsman services and the household of the individual property owner. This applies, for example, to the expansion of the general supply network or the development of a road. This position corresponds to the BFH ruling of 28.4.2020 (VI R 50/17).

(2024): Caution: Household services are not always deductible

Can I also claim the tax reduction as a tenant?

Yes, because you do not need to be the owner of the flat to claim the expenses.

Taxpayers who wish to claim tax reductions for household services or tradesmen's services do not need to be the client of the measure carried out. Therefore, tenants can also claim costs for services commissioned by the landlord and paid by them as part of the service charges.

If the landlord has commissioned household services and tradesmen's services, tenants can claim the amounts paid for service charges as tax reductions, also within the specified maximum amounts.

With the service charge statement for the flat, you can save a significant amount of tax, as many items can reduce the tax burden as household services or tradesmen's services. For service charges, this mainly concerns the items

- Garden maintenance

- House cleaning

- Caretaker activities

- Chimney sweep fees

- Lift maintenance.

Bescheinigung nach § 35a

To claim the tax benefit at the tax office, the tenant needs a certificate from the landlord containing the relevant details. The usual service charge statement is generally not sufficient for this. However, tenants have a legal right to such a certificate.

Note: If you are renting, you can also claim tax benefits for household employment or tradesmen's services if you have commissioned them yourself and they were carried out in your flat.

The Federal Fiscal Court (BFH) recently clarified that tenants can claim expenses for household services and tradesmen's services in accordance with § 35a EStG for tax purposes, even if they have not concluded the contracts themselves (BFH ruling of 20.04.2023, VI R 24/20). If the tax office requests corresponding proof, it is advisable to request a certificate from the landlord in accordance with Appendix 2 of the BMF letter dated 9.11.2016.

If the landlord refuses to issue the certificate or requests additional proof, such as tradesmen's invoices, the tenant can invoke their right to inspect documents in accordance with § 259 (1) BGB. According to the constant case law of the Federal Court of Justice, the tenant is allowed to inspect, photograph, scan or copy the documents. For price-controlled housing, § 29 (2) sentence 1 of the Regulation on the Determination of the Permissible Rent even permits the making of copies against reimbursement of costs (BGH ruling of 8.3.2006, VIII ZR 78/05).

(2024): Can I also claim the tax reduction as a tenant?

How are home office costs taken into account for tax purposes when used jointly?

When sharing a home office, for example between spouses, the following rules apply:

- The conditions for deducting home office costs are checked individually (BFH rulings of 15.12.2016, VI R 53/12 and VI R 86/13).

- If the conditions are met, each user who uses the home office as their main place of work can deduct the costs they have incurred.

- Property-related costs (e.g., depreciation, interest on loans) are deductible if they are owed by the user (BFH ruling of 6.12.2017, VI R 41/15).

- Rental costs for jointly rented rooms are also deductible, regardless of the type of partnership.

- Usage-related expenses (e.g., energy and cleaning) are fully deductible if they relate to the use of the home office (BMF letter of 15.8.2023, IV C 6 - S 2145/19/10006 :027).

Example 1: A and B use a home office equally. The total expenses amount to 4.000 Euro and are jointly borne by A and B. A uses it as their main place of work. A can deduct 2.000 Euro as business expenses. B can only claim the daily allowance of 6 Euro per day if they worked from home on those days.

Example 2a: A and B jointly use a home office in the apartment rented by B. The expenses amount to 3.000 Euro for rent and 1.000 Euro usage-related expenses. A uses it as their main place of work. A can only deduct 500 Euro (= half of the usage-related expenses). The rental expenses are attributed to B as property-related expenses because B is contractually liable for the rent. B can therefore only claim the daily allowances.

Example 2b: If, on the other hand, A pays the rent, the property-related expenses of 1.500 Euro are also deductible by A.

Example 3: A and B jointly use a home office, which is the main place of business and professional activity for both throughout the calendar year. They waive the calculation of the expenses incurred and can each deduct the annual allowance of 1.260 Euro as business expenses or income-related expenses.

(2024): How are home office costs taken into account for tax purposes when used jointly?

Pet care is also eligible as a household-related service!

Pet care can be tax-deductible as a household-related service. Expenses for household-related services are deductible from the tax liability at 20% (up to 4,000 Euro annually) according to § 35a para. 2 EStG. Initially, the tax authorities refused to recognise such costs for pets, but the Federal Fiscal Court (BFH) ruled in a landmark decision (BFH ruling of 3.9.2015, VI R 13/15) that pet care and supervision also count as household-related services.

Tax benefits for pet care

In the specific case, a couple hired a pet and house sitter to look after their house cat during their absence. The tax office refused the tax deduction, as pet care costs were not eligible according to a previous BMF letter (BMF letter of 10.1.2014). However, the BFH saw it differently: tasks such as feeding, grooming, and cleaning are regular household tasks and therefore household-related.

Conditions for tax deduction

The tax deductibility of pet care costs applies if the care takes place in the household or on the pet owner's property. Travel costs can also be deducted. However, care outside the household (e.g. dog walkers who pick up and return the pet) is generally not tax-deductible according to the courts (FG Münster, ruling of 25.5.2012, Az: 14 K 2289/11).

Interesting: Taking the pet outside the home is not considered detrimental to tax according to the BFH ruling. However, there are cases where the tax authorities reject care services, especially if the dog is extensively cared for outside the household (FG Berlin-Brandenburg, ruling of 7.11.2018, Az: 7 K 7101/16).

(2024): Pet care is also eligible as a household-related service!

Which expenses are eligible?

Eligible expenses include gross wages or salary (for "mini-jobs") and the social security contributions paid by the employer, wage tax including the solidarity surcharge and church tax, accident insurance contributions, and levies under the Expense Reimbursement Act (U 1 and U 2).

(2024): Which expenses are eligible?

Is a shared workspace a sufficient other workplace?

Taxpayers can deduct a flat rate of 6 Euro for each day on which the business or professional activity is carried out "predominantly" at home and the primary workplace is not visited. The daily allowance is also referred to as the home office allowance or homework allowance.

This applies to all employees and self-employed individuals who, like during the Corona years, occasionally work from home but have their "actual" workplace with a desk at the office or company. The deduction of the home office allowance is limited to a maximum of 1,260 Euro per year (210 days x 6 Euro).

It does not matter whether a separate study is available. A work corner is sufficient. A deduction for travel expenses alongside the home office allowance is not permitted if you work partly at home and partly at your employer's office or premises on the same day and travel costs are incurred.

A parallel deduction of travel expenses and the daily allowance is exceptionally possible only if a business trip is undertaken on a home office day.

If no other workplace is permanently available for business and professional activities, home office costs can be deducted with a daily allowance of 6 Euro per day, up to a maximum of 1,260 Euro per year.

This applies, for example, to many teachers whose main place of work is the school, but who do not have a desk there for lesson preparation and follow-up.

Important: In this case, in addition to the daily allowance, travel costs to the school, office, or company can also be deducted using the travel allowance. It no longer matters whether a separate study is available. A work corner is sufficient; in a pinch, it can even be the kitchen table. This is a real simplification compared to the previous regulation.

But what is an "other workplace" and in which cases is it "not permanently available"? The following applies:

- An "other workplace" is generally any workplace suitable for office work. No further requirements are placed on the nature of the workplace.

- Another workplace is available if you can actually use it to the extent and in the manner specifically required.

The Federal Fiscal Court has ruled that a pool workplace is generally an "other workplace", but only if the employee can actually use it to the extent and in the manner specifically required. There must be a sufficient number of pool workplaces available.

Conclusion: If you have a pool workplace, a deduction of the daily allowance is usually only permissible for days on which you do not visit the (primary) business premises or primary workplace and work predominantly at home.

(2024): Is a shared workspace a sufficient other workplace?

Which measures are subsidised and what is the amount of the tax reduction?

As part of household-related services, the work must have been carried out by a self-employed service provider or service agency. Eligible services include, for example:

- cleaning the flat, window cleaning, cleaning the stairwell and other communal areas,

- garden maintenance (e.g. mowing the lawn, trimming hedges),

- services for private moves (minus reimbursements from third parties).

An exemplary list of eligible and non-eligible household-related services and tradesmen's services can also be found in the BMF letter dated 11.09.2016.

The expenses for household-related services provided by self-employed service providers are directly deductible from the tax liability, up to 20.000 Euro with 20 percent, maximum 4.000 Euro per year.

As a rule, a prerequisite for the deduction of costs is that they are related to your own household. However, various activities are carried out both on private property and on public land, or they benefit the private household at least indirectly, even if they primarily concern the public area. These include, for example, pavement cleaning or snow clearing.

- In 2014, the Federal Fiscal Court ruled that snow clearing on public pavements is considered a privileged household-related activity. The costs for winter services in front of your own property are therefore deductible at 20 percent from the tax liability (BFH ruling of 20.3.2014, VI R 55/12). According to the BFH judges, services are related to the household if they are provided "in the spatial area of the existing household". This includes the flat as well as the associated land. Therefore, the term "household" is to be interpreted spatially-functionally.

- In 2020, however, the BFH ruled that expenses for street cleaning in front of the property are not tax-privileged as household-related services according to § 35a para. 2 sentence 1 EStG (BFH ruling of 13.5.2020, VI R 4/18).

- Currently, the Federal Ministry of Finance has published the following brief overview in line with the BFH (BMF letter dated 1.9.2021, IV C 8 - S 2296-b/21/10002 :001):

As a rule, a prerequisite for the deduction of costs is that they are related to your own household. However, various activities are carried out both on private property and on public land, or they benefit the private household at least indirectly, even if they primarily concern the public area. These include, for example, pavement cleaning or snow clearing.

- In 2014, the Federal Fiscal Court ruled that snow clearing on public pavements is considered a privileged household-related activity. The costs for winter services in front of your own property are therefore deductible at 20 percent from the tax liability (BFH ruling of 20.3.2014, VI R 55/12). According to the BFH judges, services are related to the household if they are provided "in the spatial area of the existing household". This includes the flat as well as the associated land. Therefore, the term "household" is to be interpreted spatially-functionally.

- In 2020, however, the BFH ruled that expenses for street cleaning in front of the property are not tax-privileged as household-related services according to § 35a para. 2 sentence 1 EStG (BFH ruling of 13.5.2020, VI R 4/18).

- Currently, the Federal Ministry of Finance has published the following brief overview in line with the BFH (BMF letter dated 1.9.2021, IV C 8 - S 2296-b/21/10002 :001):

(2024): Which measures are subsidised and what is the amount of the tax reduction?

Requirements for all tax reductions

The service must have been performed in the taxpayer's household. This condition is not met, for example, in the case of

- care and support for sick, elderly, and dependent persons in a day care facility,

- repair of household items at the repair company's premises,

- waste collection (the processing or disposal of waste takes place outside the household)

The household must be located in the European Union or the European Economic Area. If the taxpayer's expenses relate to several households (e.g. main residence and holiday home), the maximum amount is deductible only once in total.

Not eligible are expenses that have already been taken into account for tax reduction under other provisions of the Income Tax Act as business expenses, income-related expenses, special expenses, or extraordinary burdens.

Special feature for homeowners: Homeowners who use their own property receive the tax reduction even if the community or the administrator is the employer or client. This is done proportionally according to their co-ownership share.

Müllabfuhrgebühren

The costs for waste collection cannot currently be considered as a household-related service in your tax return. This is based on a ruling by the Cologne Fiscal Court on 26 January 2011 (4 K 1483/10, EFG 2011 p. 978 no. 11).

The reason for this is that the main service is not provided within your property boundaries. The actual service is not the collection of the waste, but its subsequent disposal and processing. The emptying and transport of the waste are considered supporting activities. The Münster Fiscal Court recently confirmed this view (ruling of 24 February 2022, 6 K 1946/21 E). However, an appeal was rejected for procedural reasons, not on substantive grounds. This means that the issue has not yet been definitively clarified.

(2024): Requirements for all tax reductions

What evidence is required for tax reduction under section 35a of the Income Tax Act?

To claim the tax reduction under § 35a EStG (household services, craftsmen's services and care expenses), certain conditions and evidence must be met.

1. Invoices and proof of payment

The service provider must issue a proper invoice, with labour and material costs listed separately. Only labour, machine and travel costs, and the VAT on these, are eligible. Payment must be made by bank transfer; cash payments are not recognised.

2. Household services and care expenses

Household services include not only traditional tasks such as cleaning or gardening but also home care for people in need of care. Since 2009, no proof of the care level is required.

3. Missing service charge statement

If you have not yet received the service charge statement for the current tax year, you can submit the previous year's statement. The year the statement is received counts.

4. Court rulings on care costs

BFH ruling of 3 April 2019 (residential care not deductible, ref.: VI R 19/17)

The Federal Fiscal Court ruled in 2019 that only costs for one's own care or accommodation in a home are deductible. If children cover the costs for their parents' residential care, this is not tax-deductible.

Ruling of the Berlin-Brandenburg Fiscal Court of 11 December 2019 (outpatient care deductible, ref.: 3 K 3210/19)

The Berlin-Brandenburg Fiscal Court ruled that costs for outpatient care of relatives are deductible if the care takes place in the taxpayer's household.

BFH ruling of 12 April 2022 (outpatient care deductible, residential care still not deductible, ref.: VI R 2/20)

The BFH ruled in 2022 that outpatient care in the parents' household is also deductible if the child is contractually obliged. Costs for residential care remain non-deductible for tax purposes.

(2024): What evidence is required for tax reduction under section 35a of the Income Tax Act?

Current decisions

Waste collection costs and other tax deductions: What applies?

Waste collection costs are currently not tax-deductible. This is based on a ruling by the Cologne Finance Court on 26 January 2011 (Ref: 4 K 1483/10). The reason: The main service, waste disposal, is not carried out on your own property but off-site, which excludes deductibility.

Why are waste collection costs not deductible?

Waste collection is considered a supporting activity. The actual service is the disposal and recycling of waste, which does not take place on the property. The collection of the waste itself is only an intermediate step and therefore not eligible.

A ruling by the Münster Finance Court on 24 February 2022 (Ref: 6 K 1946/21 E) confirmed this view. Although an appeal was rejected for procedural reasons, the issue has not yet been definitively resolved.

Interesting: The Federal Finance Court has ruled that even in the case of rent-free accommodation, such as a son using his mother's flat, the tax reduction for craftsmen's services is possible (BFH ruling of 20.04.2023, Ref: VI R 23/21). The only requirement is that the taxpayer actually runs the household and bears the costs for the craftsmen's services.

Emergency call systems: When are costs deductible?

Costs for an emergency call system are only deductible in the context of "assisted living". In senior residences, 20 percent of the costs can be deducted directly from the tax liability. This does not apply to emergency call systems in your own home, as decided by the Federal Finance Court.

Tax benefits for tenants

Tenants can also claim tax benefits under § 35a EStG, for example for household-related services and craftsmen's services. It is crucial that the tenant receives a certificate from the landlord for the relevant expenses. A template for this certificate is included in the BMF letter dated 9 November 2016.

Costs for a structural engineer: No tax deduction

The Federal Finance Court has clarified that structural calculations by a structural engineer do not fall under the tax relief according to § 35a EStG, even if they were required for craftsmen's work (BFH ruling of 4 November 2021, Ref: VI R 29/19).

(2024): Current decisions

If you use the home office for two types of income!

The allocation of expenses for the home office or the annual allowance across different activities is permitted if you have multiple concurrent occupations and the home office is the central hub for all activities. If the central point of some activities is outside the home office, you can partially deduct the costs for these activities.

However, it is also possible to allocate all expenses to a single activity if you prefer not to provide a detailed breakdown. Please note that the annual allowance is not increased based on the number of activities carried out in the home office.

For example: If you use your home office 60% for an employed activity and 40% for a commercial side activity, and the centre of all your professional activities is in the home office, you can split the annual allowance accordingly. In this case, 60% (756 Euro) would be deducted as income-related expenses and 40% (504 Euro) as business expenses. You also have the option to apply the entire annual allowance to one of the two activities to simplify the process.

(2024): If you use the home office for two types of income!

What is the tax reduction?

If the household help is employed in a regular employment relationship and you pay normal contributions to statutory social insurance, you are entitled to an exceptionally high tax reduction.

Expenses are deductible from the tax liability up to 20.000 Euro at 20 percent, maximum 4.000 Euro per year.

If the employment relationship does not exist for the entire year, the maximum amount of 4.000 Euro is not reduced by one twelfth for each full calendar month in which the conditions are not met.

(2024): What is the tax reduction?

Home office costs: Double maximum amount for two people?

As of 1 January 2023, the tax treatment of "home office" and "homework" has been redefined.

There are two scenarios (§ 4 para. 5 no. 6b and 6c EStG, amended by the "Annual Tax Act 2022" of 16 December 2022; BMF letter of 15 August 2023, IV C 6-S 2145/19/10006):

- The home office is the "centre" of all business and professional activities:

- The annual allowance of 1,260 Euro is a flat rate for expenses in the home office.

- The option to deduct the annual allowance can only be exercised uniformly for the entire year.

- The annual allowance is personal and cannot be claimed multiple times for different activities.

- The daily allowance (6 Euro per day) cannot be deducted for the same period.

- Special regulations apply for home offices shared by spouses or partners.

- Professional activity at home, but not the centre:

- The home office allowance is 6 Euro per day for a maximum of 210 days, totalling 1,260 Euro per year.

- The workplace in the home does not have to meet any specific requirements.

- The daily allowance can be split between different activities or allocated entirely to one activity, but cannot be deducted multiple times.

- In the case of a second household or deduction of costs for a home office, the daily allowance cannot be additionally deducted.

- The daily allowance is offset against the employee allowance of 1,230 Euro and requires a tax saving of over 1,230 Euro.

- Record-keeping requirement: The calendar days on which the conditions for claiming the daily allowance are met must be recorded by the taxpayer and credibly documented in an appropriate form.

(2024): Home office costs: Double maximum amount for two people?

Are the costs for waste collection also included in the eligible expenses?

Although the waste is generated at home and collected from there, the actual service of the waste collection is not the emptying of the bins, but the transport and disposal or recycling of the waste.

This takes place outside the household of the taxpayer and is therefore not eligible.

The Münster Finance Court recently confirmed this view (judgement of 24.2.2022, 6 K 1946/21 E). The appeal against this decision was dismissed - however, for procedural reasons and not on substantive grounds. So the matter is still not completely resolved.

(2024): Are the costs for waste collection also included in the eligible expenses?

Can I deduct the costs for a tradesperson in addition to the costs for my cleaner?

Yes, you can claim the invoice for craftsmen's services (wages) and the wages for your domestic help simultaneously in the tax return. In addition to the wages for domestic help, you can also deduct the wages for craftsmen up to 6,000 Euro at 20 percent, a maximum of 1,200 Euro per year, directly from the tax liability.

Tax benefits apply not only to regular renovation work but also to one-off maintenance and modernisation measures - and not just in the home, but also on the property. The benefits apply not only to work that could usually be done by household members but also to work that can only be carried out by professionals, e.g. repairing a washing machine. The important thing is that the repair of the machine takes place in your household.

(2024): Can I deduct the costs for a tradesperson in addition to the costs for my cleaner?

What is the difference between employment and services?

A household employment exists if you or the homeowners' association have employed someone to perform household tasks for the homeowners' association. The homeowners' association is the employer of this person.

A household service exists if household tasks are carried out by a company. The homeowners' association is the client of the service.

(2024): What is the difference between employment and services?

When is employment in a private household subject to social insurance contributions?

There may be various reasons for employment subject to social security contributions for a domestic help:

- Wages over 538 Euro/month

- Multiple mini-jobs with total wages over 538 Euro/month.

In principle, there are no special features for the taxation and social security contributions of household-related wages. As in the commercial sector, the employer must withhold income tax according to the employee's electronic income tax deduction characteristics (ELStAM) and pay it to the tax office.

If you employ a domestic help subject to social security contributions or a self-employed service provider, you can claim 20 percent of the costs, up to a maximum of 4.000 Euro per year. This also applies to care and support services for a dependent relative.

Example

If you have registered a domestic help subject to social security contributions, the tax office will deduct 20 percent of the expenditure of 12.000 Euro per year from the tax liability, i.e. 2.400 Euro.

(2024): When is employment in a private household subject to social insurance contributions?

What additional levies are incurred on top of earnings?

For a part-time household employee, the employer must pay a flat rate of 12% on the wages, consisting of 5% each for statutory pension and health insurance, and 2% for tax. Additionally, the following contributions are payable in 2019:

- U1 levy for sickness and convalescence expenses: 1.1%

- U2 levy for maternity expenses: 0.24%

- Contribution to statutory accident insurance of 1.6% of wages.

- Private households do not have to pay the U3 levy for insolvency payments.

For part-time employees in private households, the private employer must use the so-called household cheque. The household cheque offers you significant relief - which you must use! And only by using the household cheque procedure can you benefit from the tax reduction under § 35a EStG. With the household cheque, you can easily register your part-time household employee with the Minijob Centre (Deutsche Rentenversicherung Knappschaft-Bahn-See) and at the same time grant a direct debit authorisation for the deduction of social contributions.

The Minijob Centre will issue an employer's business number if not already available, calculate the additional costs (flat rate, levies, accident insurance) and debit the total amount from your account twice a year by direct debit: for the first half of the year on 31 July and for the second half of the year on 31 January of the following year.

(2024): What additional levies are incurred on top of earnings?

Household-related services: Are costs for emergency call systems tax-privileged?

Expenses for a home emergency call system may be tax-deductible, depending on the circumstances:

-

As part of "assisted living" in a retirement home, the costs for a home emergency call system are tax-privileged. You can deduct 20 percent from the tax liability. This is in accordance with the Federal Fiscal Court (BFH) ruling of 3.9.2015 (VI R 18/14).

-

If the home emergency call system is used outside of "assisted living" in a retirement home, for example in your own flat, the costs are not tax-privileged.

-

The Federal Fiscal Court (BFH) recently ruled in favour of the tax authorities regarding the second case: Expenses for a home emergency call system that merely establishes contact with a service centre (on-call service) are not tax-privileged as household-related services if the service is provided outside the client's household. This is according to the BFH ruling of 15.2.2023 (VI R 7/21).

The main service of a basic home emergency call system is to handle alarms and notify contacts, the family doctor, care service, etc. by phone, not for the pensioner to call the emergency service themselves. Since this key service is not provided in the pensioner's household, it is not tax-privileged.

(2024): Household-related services: Are costs for emergency call systems tax-privileged?

Tax bonus for locksmith services?

The front door clicks shut behind you – and suddenly you're standing outside without a key. You need a locksmith. Unscrupulous companies exploit the emergency situation and demand exorbitant amounts. The question is whether at least the tax office provides some relief. Are these household-related services, which can be deducted directly from the tax liability at 20%, up to a maximum of 4,000 Euro per year (§ 35a para. 2 EStG)?

Currently, the Federal Government, represented by Parliamentary State Secretary Dr Meister, states that expenses for a locksmith to open the front door may be tax-deductible as a household-related service. This "depends on the specific service provided in each individual case. The term 'in the household' should be interpreted spatially-functionally" (BT-Drucksache 18/11220 of 17.2.2017, Question 19). The question was clear and simple, but the answer is unclear and convoluted. It is undisputed that the locksmith's service is provided in the spatial area of the household, which is defined by the property boundaries. This also includes the front door or apartment door.

Never pay cash

It would have been more useful if Dr Meister had pointed out a problem: The tax benefit is only available if an invoice is issued and paid by bank transfer. That's the theory. But in practice, locksmiths usually want immediate payment, preferably in cash. You can consider yourself lucky if the locksmith at least provides a receipt (but cash receipts are not accepted by the tax office!). It's better to be persistent and insist on a bank transfer. You can also offer the locksmith an immediate transfer via online banking – once you're back in the flat.

(2024): Tax bonus for locksmith services?

Sichern Sie sich einfach die volle Steuererstattung, die Ihnen zusteht!

Nur Lohnsteuer kompakt bietet Ihnen:

- Persönliche Steuertipps im Wert von 312 Euro (Durchschnitt)

- Verständliche Eingabehilfen und Erklärungen

- Import aus jeder beliebigen anderen Steuersoftware

- Schnelle Antworten bei Fragen

Jetzt kostenlos testen